In order to promote employment and relieve financial hardship caused by the COVID-19 outbreak, the Ministry of Finance has announced tax exemptions and reductions for goods and services under the Excise Tax Act BE 2560 (2017). The Ministerial Regulation was promulgated in the Government Gazette on July 8th, 2020 and came into force the next day.

The goods and services entitled to excise tax exemptions and reductions include three-wheeled electric vehicles, tobacco products, entertainment and recreational businesses, horse racing tracks, and golf courses.

Three-wheeled electric vehicles

To promote the electric vehicle industry, the excise tax rate on three-wheeled electric vehicles has been reduced to 2% ad valorem. The excise tax on non-electric three-wheeled vehicles remains at 4% ad valorem.

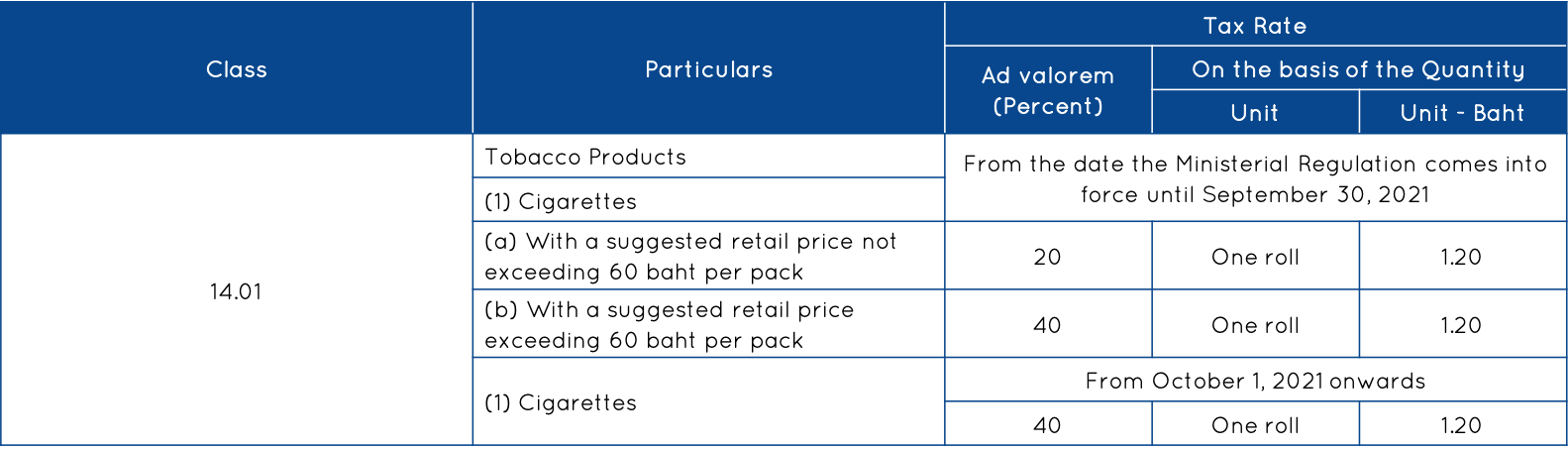

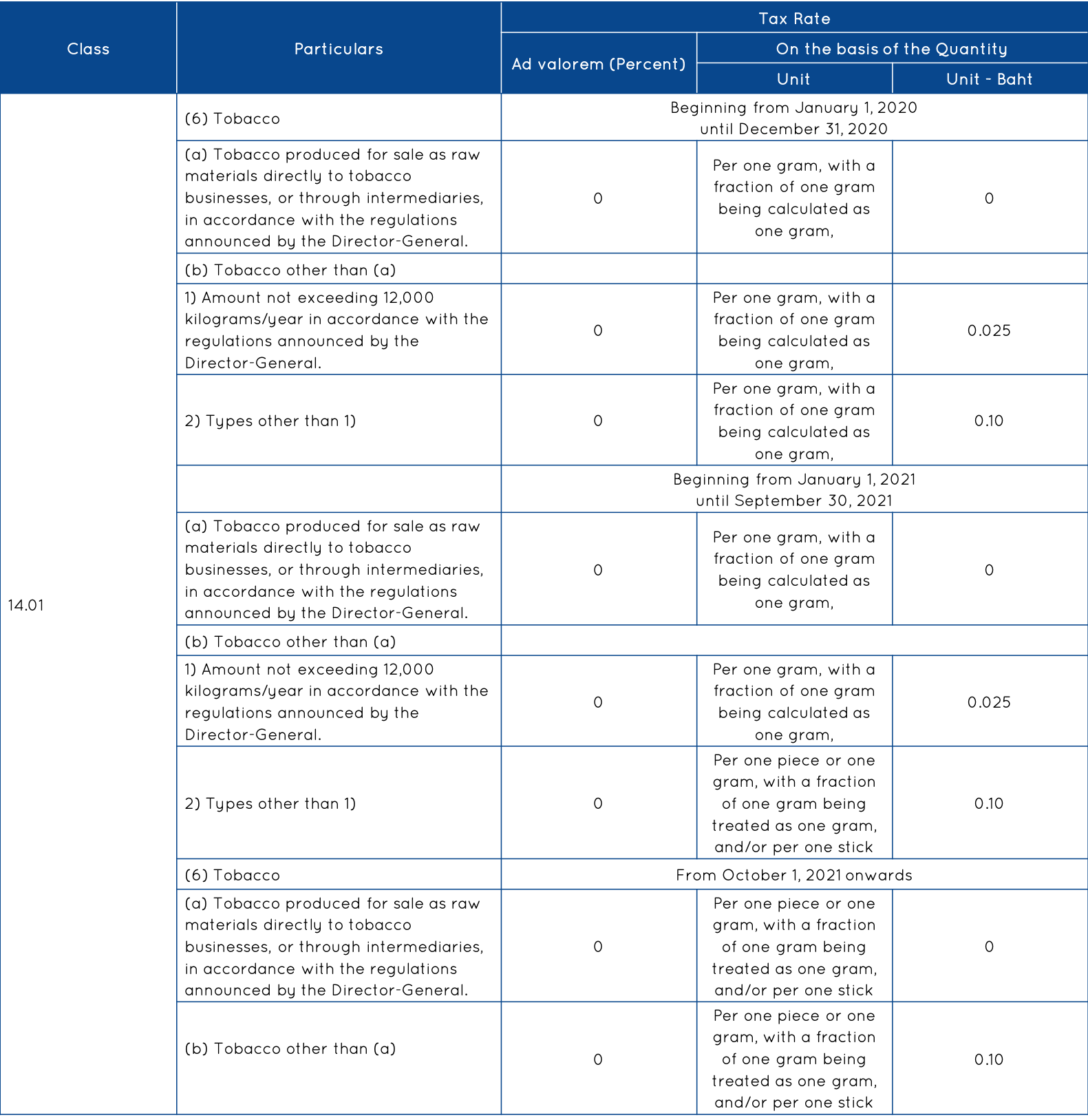

Tobacco products

The current excise tax rates imposed on tobacco and cigarettes are extended until September 30th, 2021. Higher tariff rates will come into effect on October 1st, 2021.

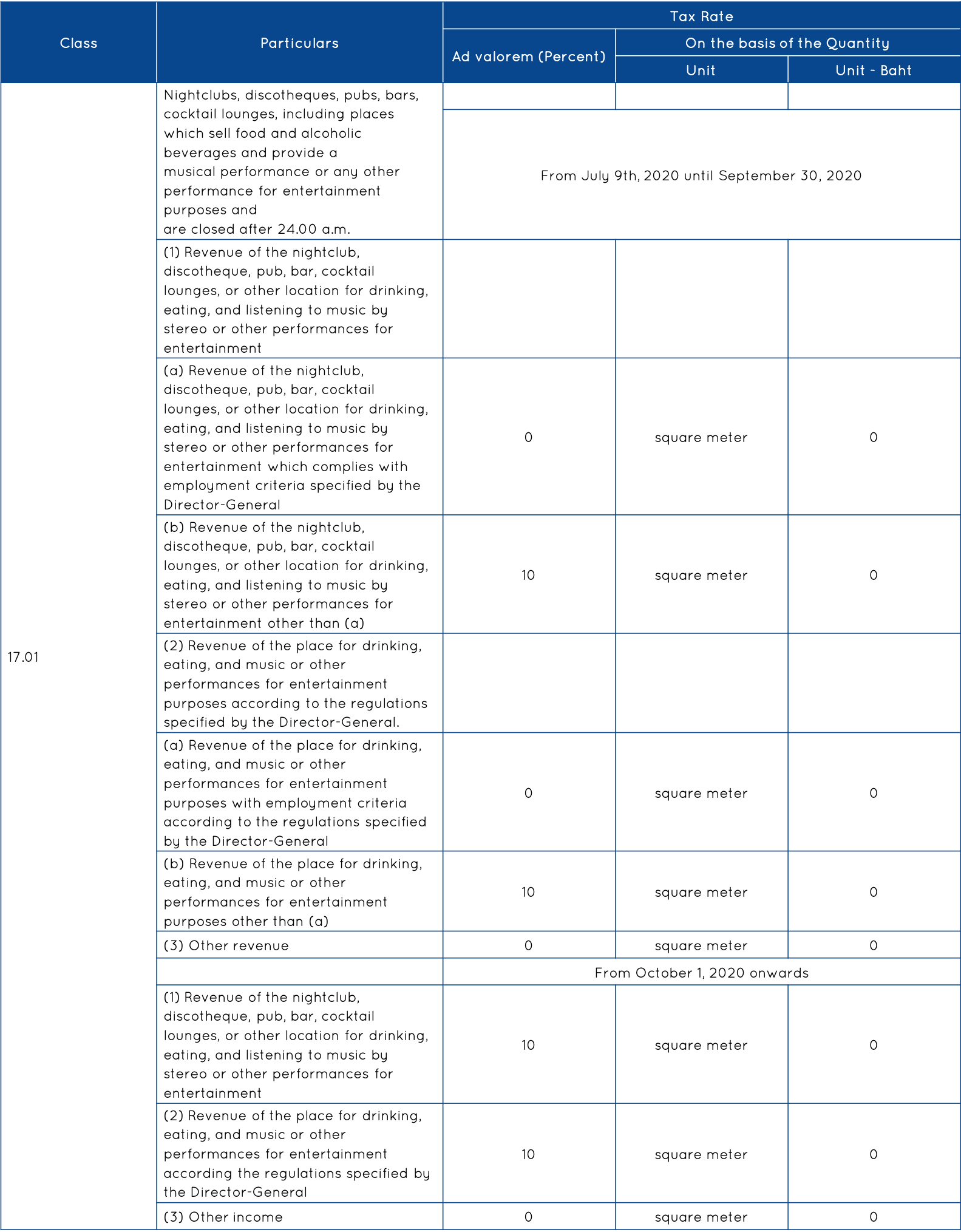

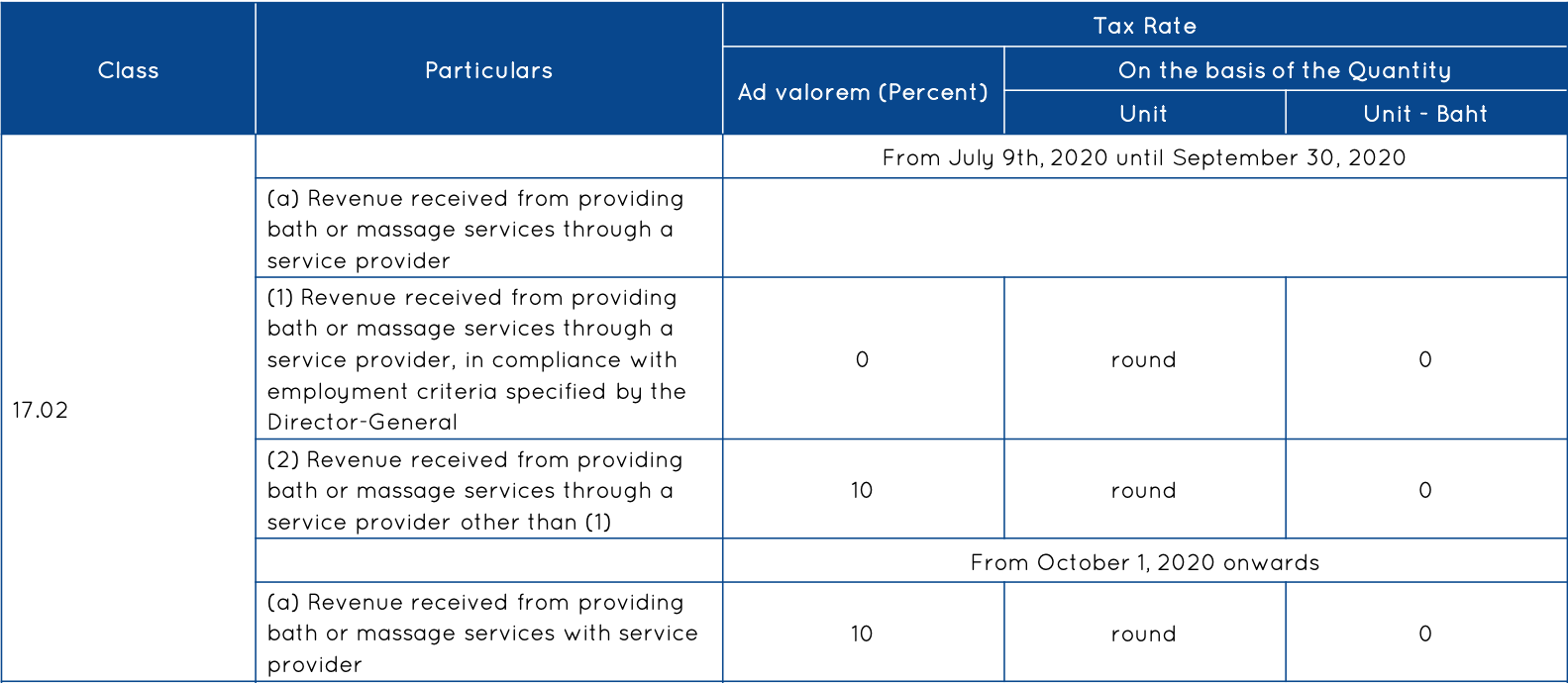

Entertainment and Recreational Businesses

To encourage businesses to retain employees, entertainment and recreational businesses — such as nightclubs, bars, and massage parlors — who maintain their level of employment in accordance with criteria issued by the Director-General are entitled to a 0% excise tax rate until September 30th, 2020. Other businesses of this category will be subject to a reduced 10% ad valorem tax rate. After October 1st, 2020, all businesses will be subject to a 10% ad valorem tax rate.

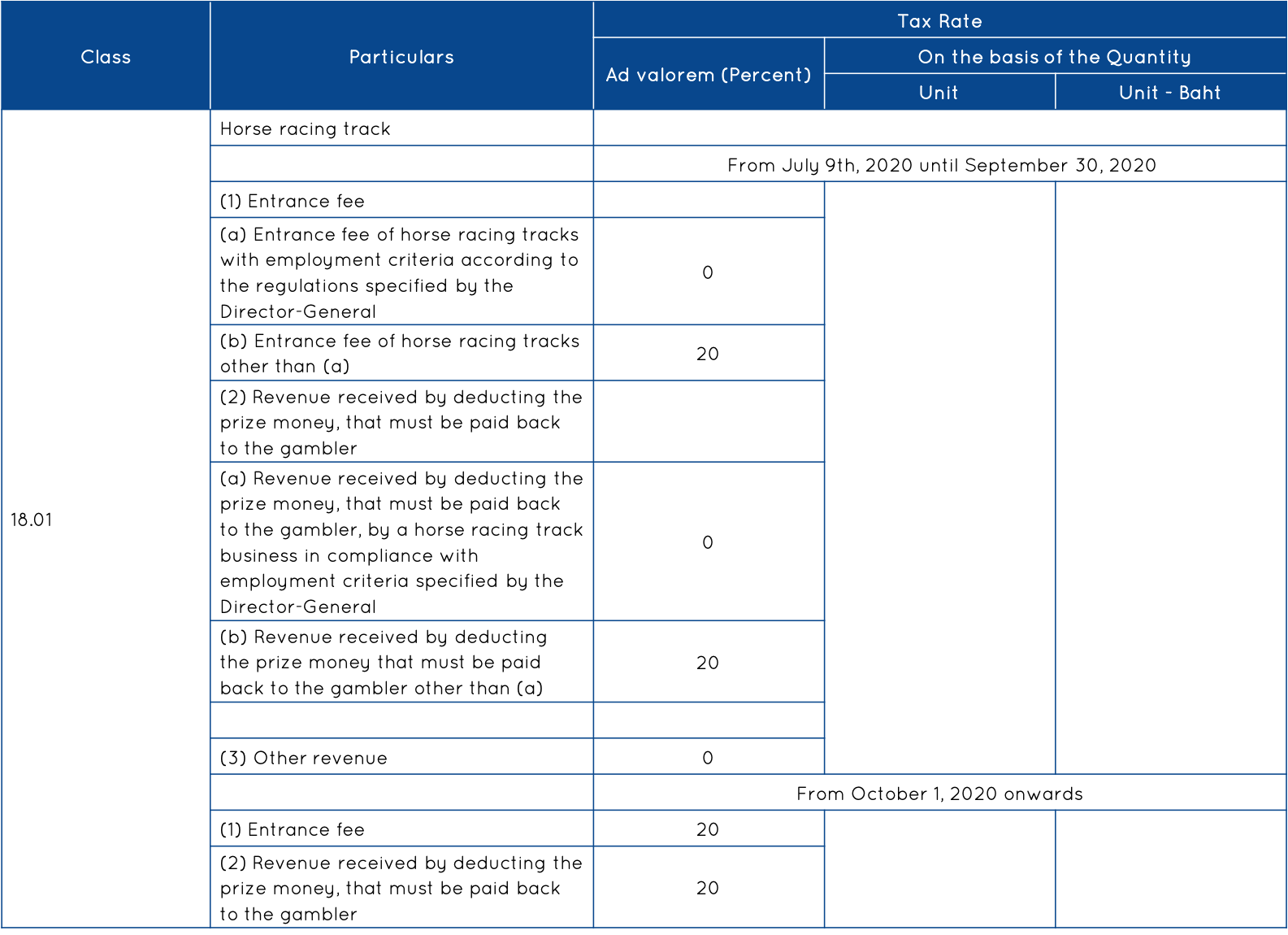

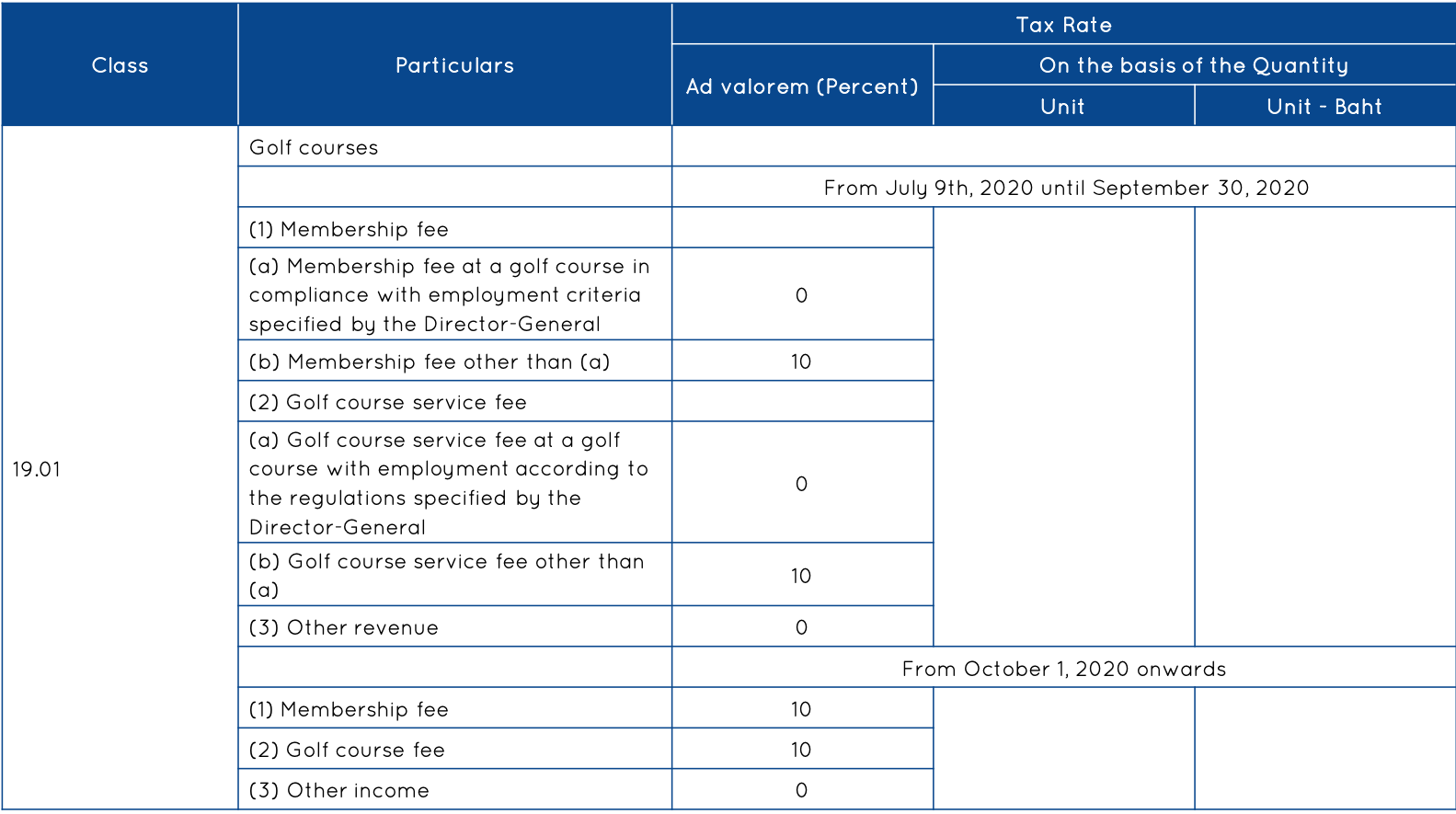

Horse Racing Tracks and Golf Courses

For horse racing tracks, entrance fees and revenue received through prize money deductions will not be subject to excise tax until September 30th, 2020, provided that the business maintains their level of employment in accordance with criteria issued by the Director-General. Otherwise, entrance fees and the aforementioned revenue are subject to tariffs at a rate of 20% ad valorem. From October 1st, 2020 onwards, both will be taxed at a 20% ad valorem rate.

Similarly, membership fees and golf course service fees at golf courses that have maintained their employment levels in accordance with criteria prescribed by the Director-General will not be subject to excise tax until September 30th, 2020. If the business is ineligible under the Director-General’s criteria, it will be subject to a reduced 10% ad valorem rate. From October 1st, 2020 onwards, all membership fees and golf course fees will be subject to excise tax at a rate of 10% ad valorem.