Introduction

Despite bursts of public health recovery in many countries and nascent hopes for a vaccine, the global economic outlook for COVID-19 continues to be dire, with the OECD predicting in June that GDP in 2020 would fall by at least 6.0%, and trade volume by at least 9.5%.

One area of damage with particularly diverse effects has been the disruption to international trade. In addition to supply chain disruptions due to industrial shutdowns and delays in shipping and transport, other logistical issues include disruptions in the delivery of trade finance documents due to the lingering problem of paper-reliance in international trade. Trade and trade finance operations involve a large volume of paperwork—such as bills of lading, letters of indemnity, packing lists, certificates of origin, proforma invoices and so on—traditionally exchanged in physical form. It is paramount that trade documentation is not only correct and complete, but also delivered to the right party at the correct time. The problem of pandemic-related delays in the delivery and processing of trade documents, due to reduced staffing and limited postal or courier services, prompted the International Chamber of Commerce (ICC) to release a memo in April 2020 imploring banks and central governments to lift all legal prohibitions on the use of electronic trade documentation and support a swift transition to paperless trading. More recently, in July 2020, the World Trade Organization, the ICC, and B20 Saudi Arabia jointly issued an industry-wide call for increased cooperation between public and private sectors in order to address the trade finance shortage, including easing regulatory constraints on and implementing digital solutions for trade finance documentation.

Aside from calling attention to the need for digitalization, the pandemic’s disruption of trade finance transactions has, as in other industries, prompted discussion about the applicability of force majeure. Broadly defined, a force majeure clause is a contractual clause wherein a party or parties to a contract are unable to perform their obligations due to an extraordinary and unforeseeable event, beyond their control, which prevents or precludes them from performing their contractual obligations. In common law jurisdictions, such as the UK, parties may not avail themselves of the force majeure doctrine unless their contract contains a force majeure clause. Conversely, in civil law jurisdictions, like Thailand, the force majeure doctrine is generally recognized, meaning that even if a force majeure clause is not included in a contract, the local statutory provision may still apply on a case-by-case basis (in Thailand, force majeure is defined in Section 8 of the Commercial and Civil Code). Including a tailored force majeure clause in contracts is recommended in order to avoid the limitations of the relevant local law and its interpretation by the courts.

In this article, we will take a look at the ICC’s response to COVID-19 and the question of force majeure, as well as considerations for force majeure under trade finance instruments.

The ICC’s Updated Force Majeure Clause

As of March 2020, ICC has updated their model force majeure and hardship clauses in response to the pandemic. The ICC’s model clauses are designed for use in commercial contracts, and should be tailored to the unique requirements of the parties involved.

The ICC now offers two versions of the force majeure and hardship clauses—a long-form and short-form clause. As the ICC notes, the long-form clause offers more protection.

Furthermore, in response to the protracted and unpredictable nature of the pandemic, the updated force majeure clause establishes a specific duration of the impediment before the contract is terminated, stating that parties may terminate the contract if the impediment exceeds 120 days. The prior version of the clause allowed either party to terminate the contract if the impediment persisted for a “reasonable period” of time.

Like the 2003 version of the clause, the ICC’s 2020 contractual force majeure clause provides both an open-ended definition and an itemized list of events (“presumed force majeure events”) which commonly qualify as force majeure, including war, natural disasters, plague, currency and trade restrictions, and so on. Under the ICC’s open-ended definition, the affected party who wishes to claim force majeure must prove the following:

✓ that the impediment is beyond its reasonable control; and

✓ that it could not have reasonably foreseen the impediment at the time of the contract; and

✓ that it could not have reasonably avoided or overcome the effects of the impediment.

In the presence of one or more of the “presumed” events, the affected party will only need to prove the last condition (i.e. that the effects of the event could not have been reasonably avoided or overcome).

The broadness of the ICC’s definitions means that situations will be analyzed on a case-by-case basis, and whether COVID-19 is considered as force majeure in issues of contractual non-performance is left to the interpretation of the court.

The ICC on Trade Finance Instruments

For trade finance instruments, force majeure is defined in each of the following ICC rules: the Uniform Customs and Practice for Documentary Credits (UCP 600), the Uniform Rules for Demand Guarantees (URDG 758), the Uniform Rules for Collections (URC 522), the Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits (URR 725), the UCP and URC eRules (eUCP Version 2.0 and eURC Version 1.0) and the Uniform Rules for Bank Payment Obligations (URBPO 750). Generally speaking, the provisions describe force majeure as an event interrupting the bank’s business that is beyond the bank’s control. This offers the banks some protection, but force majeure is unlikely to be triggered under trade finance instruments, as it is rare that documents are impossible to be delivered or processed.

In a guidance paper published in April 2020, the ICC suggests, by way of reference to its stance on the 2010 Icelandic volcano eruption, that the pandemic in itself is unlikely sufficient to qualify as a force majeure event. However, the ICC stresses that it cannot provide authority on whether an event qualifies as force majeure, even when a trade finance transaction is governed by its rules, as the question remains for the relevant governments, courts and tribunals, and regulatory authorities to decide. Furthermore, the guidance paper cautions that if the performance of an obligation or contract is not impossible, only more difficult or expensive, then the event may not constitute force majeure under ICC rules.

To mitigate the pandemic’s impact and avoid disputes, the ICC advises businesses and banks to focus on implementing business continuity plans and engage in open communication between parties. In particular, the ICC rules relevant to a transaction may be modified with the agreement of all parties involved—for instance, in order to allow for delays in documents or demands, parties may agree to extend certain periods—and physical document transmission may be replaced by digital solutions.

Force Majeure and Considerations for Trade Finance Instruments

COVID-19 may constitute a force majeure event. However, in relation to trade finance instruments, such as letters of credit and demand guarantees, which are used to ensure that a payment or performance is carried out, the question of force majeure will be dealt with separately from how it is treated under the contract for the sale and export of goods. In other words, the question of force majeure under the terms of a trade finance instrument is considered separately from a force majeure event under the underlying contract.

This is because trade finance obligations are independent of the underlying contracts or undertakings that they are issued to underpin. For instance, although there is a cause-and-effect relationship between a contract for the sale and export of goods and the letter of credit that is issued to secure payment for the same, the two contracts and their respective obligations are independent of the existence and performance of the other. In a trade finance transaction, the bank will not inspect the goods or the underlying sale contract; it will only deal with the documents that are presented, and will honor them as long as they are in compliance with the terms of the credit.

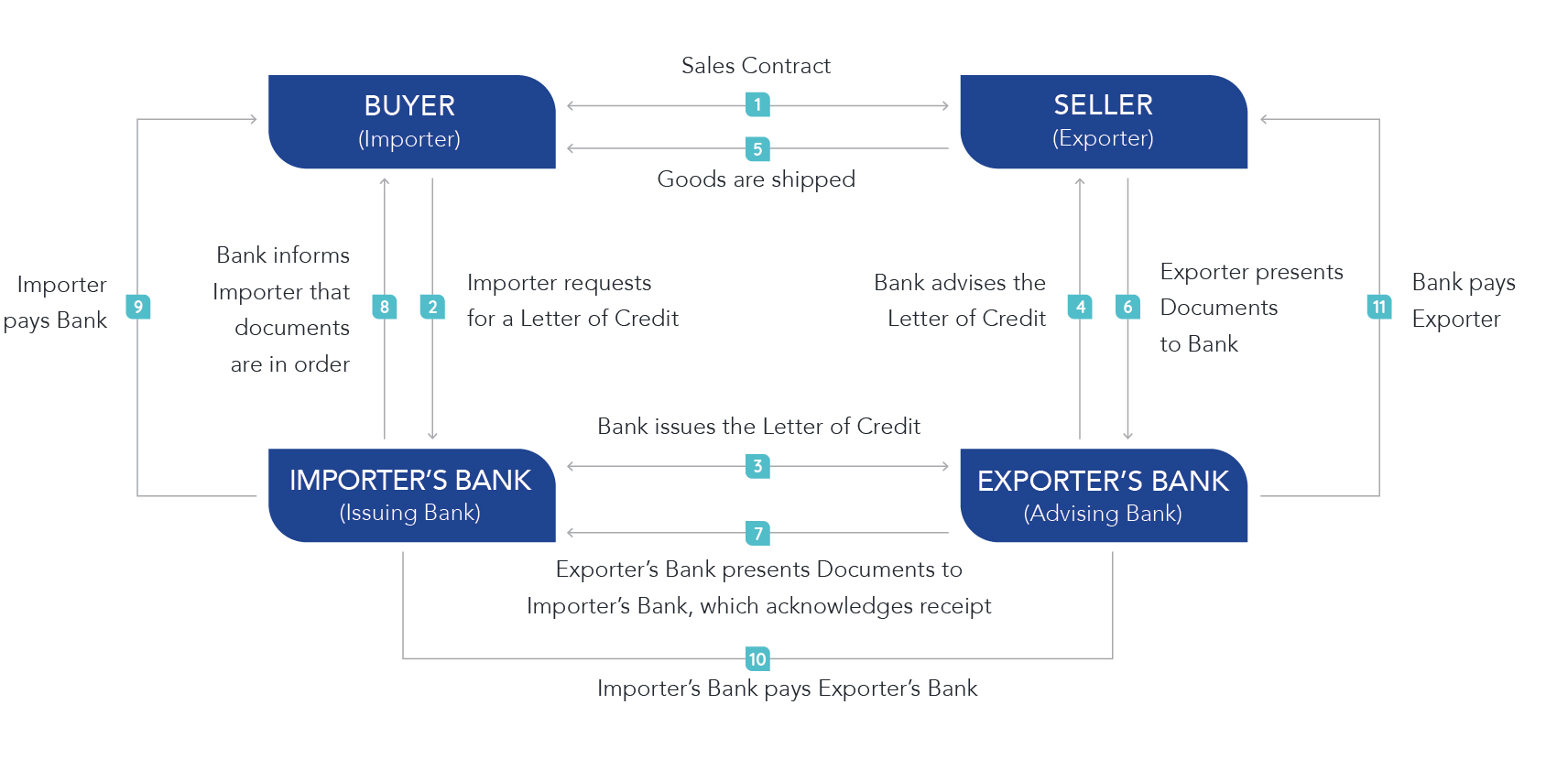

Letters of credit

The New York Uniform Commercial Code states that Letters of Credit must satisfy formal (“documentary”) requirements, but that the “rights and obligations of an issuer to a beneficiary or a nominated person under a letter of credit are independent of the existence, performance, or non-performance of a contract or arrangement out of which the letter of credit arises or which underlies it, including contracts or arrangements between the issuer and the applicant and between the applicant and the beneficiary.” Similarly, the ICC Uniform Customs and Practice for Documentary Credits (UCP 600) underscores the independence of letters of credit, which must be honored by a bank regardless of the performance or non-performance of the underlying obligation, even in the event that non-performance depends on a force majeure event.

In fact, unlike negotiable instruments, which are unconditional promises for payment, L/Cs are conditional to the presentation of complying documents by a beneficiary. Therefore, if a force majeure event affects the performance of an exporter to ship the agreed-upon goods, whose quantity and quality comply with the terms of the sales agreement, but the business of the issuing or confirming bank is not impaired, then the bank will honor the documentary credit.

Demand guarantees

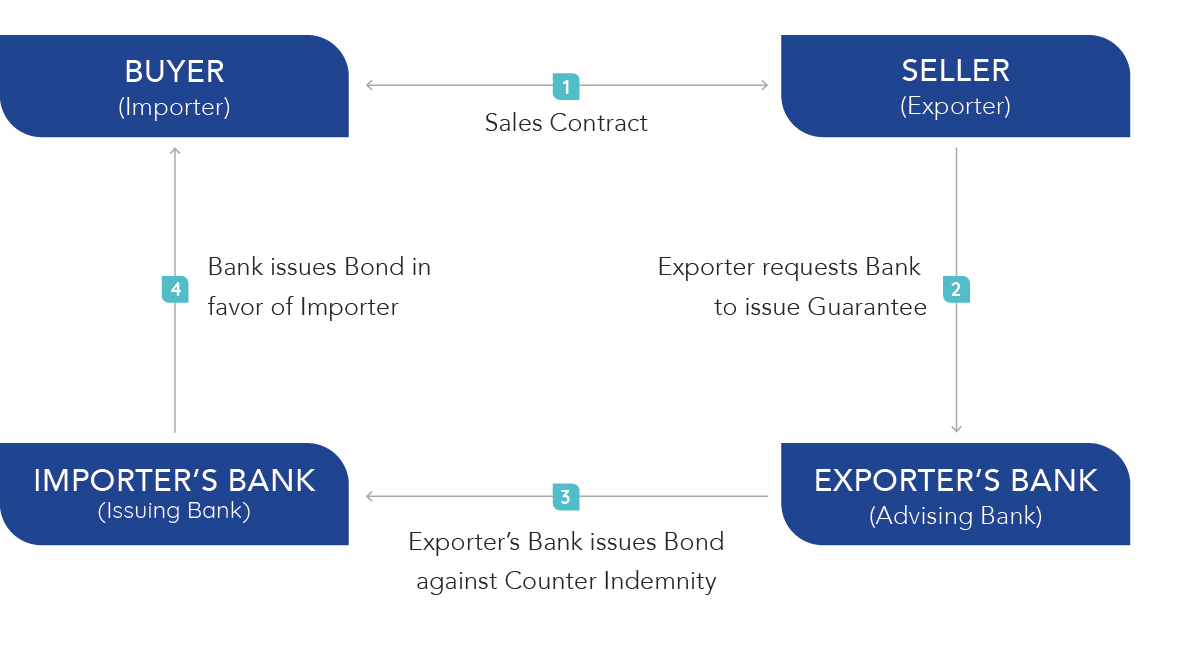

Likewise, demand guarantees (regulated by the URDG 758) and stand-by letters of credit (regulated by the ISP 98) are independent contracts, separate from their underlying contracts and independent of the underlying transactions.

Art. 26 of the Uniform Rules for Demand Guarantees (URDG) of the International Chamber of Commerce (ICC), publication no. 758, defines Force Majeure as “acts of God, riots, civil commotions, insurrections, wars, acts of terrorism or any causes beyond the control of the guarantor/counter-guarantor.” In the event a demand guarantee expires at a time when a documentary presentation is impossible due to force majeure, the guarantee (and counter-guarantee, if any) is extended once by 30 calendar days. Nevertheless, even if a guarantee has expired due to a force majeure event, the beneficiary can demand its enforcement after termination of the event, which could not reasonably have been avoided or overcome. Furthermore, no interest will be due to the beneficiary in case of payment suspension or guarantee expiration due to force majeure.

Similarly, a claim for the respective counter-guarantee may be presented within thirty calendar days after termination of a local force majeure event, even if it has expired. For instance, if a counter-guarantee issued by a bank in Japan for a bank in Thailand expires at a time when its presentation is not possible due to COVID-19, it is extended by 30 calendar days from the date on which the Japanese bank notifies the Thai bank about the termination of the force majeure event. The demand will be paid after termination of the force majeure event, even if the demand has expired.

Conclusion

As the pandemic has shown, there are many contingencies that can affect trade; therefore, it is advisable for trade operators to be prepared for worst-case scenarios and to not rely on good-faith. For instance, parties should be vigilant about drafting force majeure clauses tailored to their specific agreement, and avoid inserting standardized clauses into their contracts, rather than waiting until the contract fails to give the clause its due attention.

In terms of remedial measures, parties to a contract are advised to review the relevant ICC rules and trade finance instrument’s terms to explore solutions to problems. Exporters and importers should be aware that the terms of a trade finance instrument may be modified, and it is recommended to seek legal counsel from a lawyer with extensive banking experience to mitigate risks and ensure successful transactions.