As the Thai Government’s Board of Investment looks to attract foreign investors in its ambitious development efforts for Thailand’s Eastern Economic Corridor, the time is ripe for exploring some of the financial means and risk management strategies necessary to achieve the required scale. To that end, Chicago, Illinois based Arthur J. Gallagher & Co. (“Gallagher”), one of the world’s largest insurance brokers and risk management consultants, has partnered with Bangkok-based corporate financial advisory firm, Mahanakorn Partners Group (“MPG”), to educate global lenders and equity investors alike on best in class approaches to foreign direct investment in the ASEAN region.

Recently, Gallagher’s U.S. Trade Credit and Political Risk practice niche leader Marc Wagman interviewed his veteran colleague and preeminent global expert on structured credit and political risk, Gabe Mansky, on one particularly relevant strategy for financing large government sponsored infrastructure projects such as those envisioned for the Eastern Economic Corridor – the “Buyer Credit” approach.

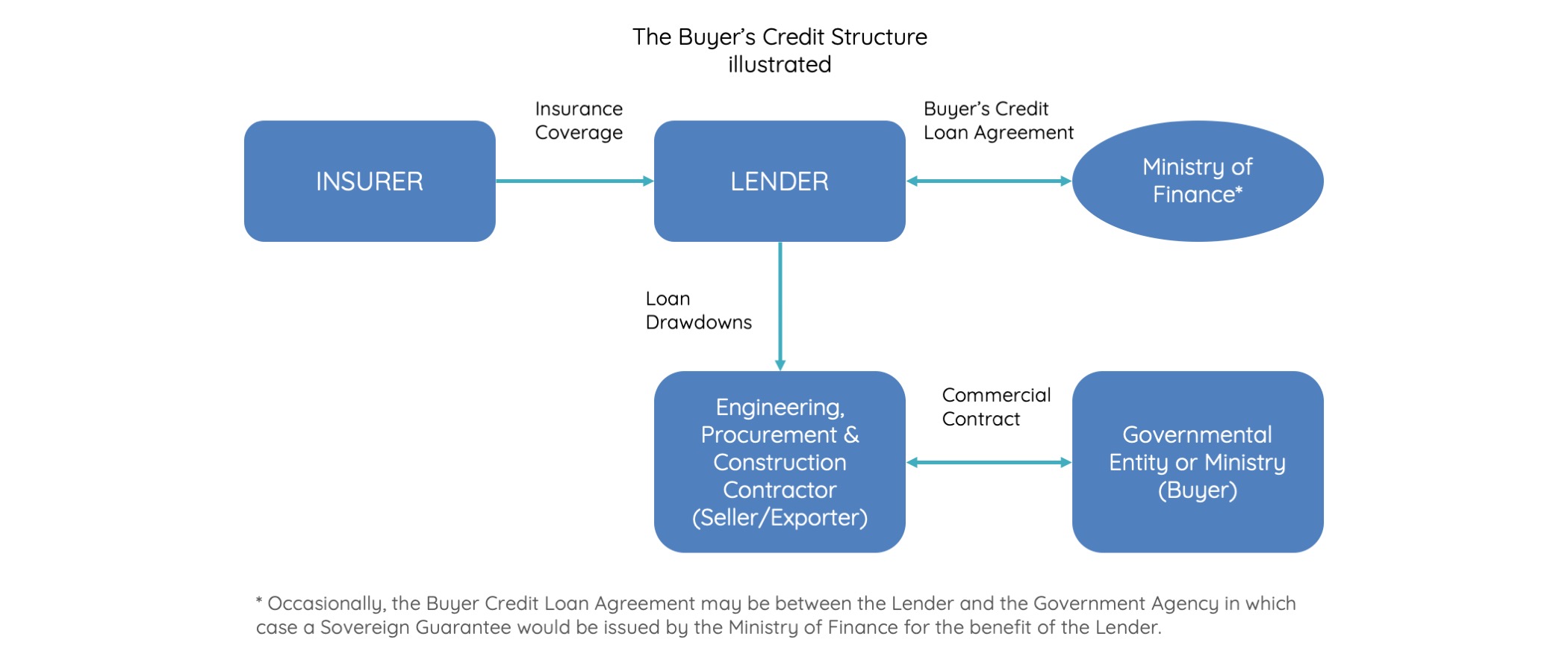

WAGMAN: What in particular is it about the Buyer Credit financing structure that makes it so unique?

MANSKY: It’s the fact that two parallel agreements are in effect when the financing transaction is consummated and yet the two agreements are completely divorced from each other. The first is the contract between the buyer (say the Ministry of Transportation, Energy or Defense) and the seller/exporter (e.g. an Engineering and Procurement Contractor). The second is the loan agreement between the Seller/Exporter and the lender. The loan agreement is the subject of the insurance coverage which at its core is protecting the lender from the non-honoring of a sovereign guarantee or a sovereign obligation.

WAGMAN: Why are Buyer Credit structures the most effective way of financing large infrastructure projects in emerging markets?

MANSKY: There are a number of compelling reasons underscoring this approach. For starters, perhaps the best way to think of this is in terms of what the mostly likely alternative to a Buyer Credit structure would be – that being where the seller/exporter has to either finance this transaction themselves or find an institution willing to finance the transaction based upon the credit quality of the seller. In that latter scenario, the loan agreement between seller/exporter and the loan itself must be sold to an investor or group of investors in the secondary market. This is a much more challenging and complicated undertaking. Following to that, one key advantage to the Buyer Credit structure is that beyond the required sovereign guarantee (most typically the host country’s Ministry of Finance), there are no collateral or security requirements needed for the lender (unlike some other trade or project finance structures). In fact, the market for this type of approach has become so commonplace that there is now a considerable degree of uniformity on the insurance policies which provide the non-payment protection underlying these loan agreements. With the input of both insurers and brokers, these insurance policies have since become recognized under both Basel II and Basel III Accords, depending upon the country.

Another benefit to the Buyer Credit approach is that neither the bank lender nor the seller/exporter pay the premium. We’ve developed a mechanism whereby the premium is embedded in the loan agreement, very typically under a line entitled “Risk Mitigation Fee” or something similar to that. So in effect it’s the Buyer who pays the premium which is effectively financed over the term of the loan but disbursed upon loan consummation and paid to the insurer(s) in full and upfront. In the loan agreement, you’ll see reference made to “principal, interest and risk mitigation fee”. All of this said, the Buyer Credit structure only makes sense for a trade related opportunity (i.e. purchase and sale of goods and/or services) or turnkey arrangements where upon completion of the project, the title to the project transfers completely to the buyer.

WAGMAN: Thailand boasts a respectable investment grade sovereign rating from Moody’s of Baa1. Does this diminish the need for political risk insurance from the lender’s point of view?

MANSKY: Not at all for any number of reasons. Firstly, many large and medium sized European and Japanese banks obtain capital relief from their regulators for mitigating the credit and political risk of their loan portfolios and credit exposures in general, even for investment grade obligors. Secondly, even in instances where the regulatory capital relief is either minimal or not applicable at all, the ability to improve the credit quality of the underlying loan by substituting that of the Buyer’s with that of the insurer(s)’, any of whom are going to have a Moody’s rating (or Standard & Poor’s equivalent) which is at least 2 or 3 notches higher, is often more than enough to persuade an infrastructure lender’s credit committee that the incremental cost of the insurance is worthwhile, especially if it can be passed onto the Buyer and financed.

WAGMAN: What are a few of the biggest challenges from the perspective of an insurer in determining the project’s underwriting feasibility?

MANSKY: First and foremost would be the available capacity for the target country in the global credit and political risk insurance markets. This is a function directly of the underwriters’ perception of the target country’s sovereign credit rating, its judicial system’s reputation for upholding the contractual rights of foreign creditors and last but not least, its macroeconomic and political stability.

Secondly, is the project deemed to be important enough to be budgeted by the country’s Ministry of Finance? If not, the likelihood of obtaining underwriting support can quickly diminish, especially in a challenging country. However if the project is budgeted, it’s axiomatic in our business to say that one can find good deals to underwrite even in very difficult countries. As just one example, we have extensive experience in securing substantial amounts of coverage with this type of financing structure in countries as difficult as Zambia, even shortly after it was downgraded to a Moody’s Caa1. Despite being 7 notches below investment grade, Zambian sovereign credit risk was underwritable for the right project and structure.

Thirdly, who is the supplier/seller/exporter? What is their experience in the country? How long have they been doing work in that country? Does this seller have the resources and ability to provide top notch management, maintenance, training and spare parts, etc.?

ABOUT THE AUTHORS

Marc D. Wagman

Before selling his company to Arthur J. Gallagher & Co. in February 2015, Marc D. Wagman was for 11 years the Managing Partner of Aequus Trade Credit, a specialty broker of credit protection products. With more than 20 years of experience in credit risk mitigation, the capital markets and commercial finance, Marc is a global leader in his field. Prior to founding Aequus in 2003, Mr. Wagman was a business development executive for Euler Hermes. In the early 1990s, he sourced distressed assets for Avenue Capital, an NYC based hedge fund. Marc began his career as a financial analyst for The CIT Group, Inc., where he co-managed CIT’s interest rate swap portfolio and received formal credit training.

Gabe Mansky

With 30 years of experience, Gabe Mansky is a senior member of Gallagher’s Trade Credit and Political Risk team and also a recognized global leader in this niche. Gabe’s responsibilities include the production, marketing and placement of large complex credit and political risk solutions. His team has successfully placed business in difficult markets such as Latin America, Central Asia, sub-Saharan Africa and Eastern Europe. Before joining Gallagher in 2008, Gabe was with Acordia/Wells Fargo Insurance Services for 11 years where he served as Head of the Trade Credit and Political Risk Practice Group in New York City. Prior to that, he was with the Credit International Associates Inc. (which ultimately became part of Aon Trade Credit) where he served as a Producer for 9 years.

THE MPG-AJG ALLIANCE

In 2018 US-based global insurance brokerage and risk management services firm, Arthur J. Gallagher, and the Mahanakorn Partners Group (MPG), ASEAN’s leading professional services firm, entered into a partnership to enhance and complement the range of corporate services that each brings to the table in support of multinational enterprises in their Foreign Direct Investments (FDIs).

Arthur J. Gallagher’s (NYSE ticker ‘AJG’) was established in 1927 and is one of the world’s largest insurance brokers, offering risk management and consulting services across a broad spectrum of coverage lines. For the ninth year in a row, Gallagher was designated by the Ethisphere Institute—a global organization that defines and measures corporate ethical standards, recognizes companies that excel, and promotes best practices in corporate ethics—as one of the World’s Most Ethical Firms. Further, in 2018, Forbes similarly recognized Gallagher as one of the World’s Best Employers. Gallagher was the only insurance broker so honored in both cases. Gallagher’s credit and political risk team has offices around the globe, differentiating itself with a unique skill set, covering both the capital markets and the credit insurance markets. The practice group consists of more than forty professionals worldwide, many of whom come from investment banking, commercial banking and corporate finance or credit backgrounds. Arthur J. Gallagher is the fastest growing insurance firm in the Fortune 500, fueled by both strong organic and aggressive mergers and acquisitions (M&A) led growth. The company is also investing in emerging business opportunities, such as clean energy, latter of which continues to be accretive to earnings while generating cash used to support the ongoing M&A activity.

The objective of the MPG-AJG Alliance is for each firm to enhance the other’s economic activities by providing international investors and enterprises with support and advisory services to achieve credit enhancement, risk mitigation and guarantee-backed lines of credit.